Measuring the Digital Economy – It’s Harder & More Important than You Think

If you left your home in the morning and realized 5 minutes later that you had forgotten to pack your smartphone, would you return home to get it? A surprisingly large amount of us probably would, given that device’s centrality to our daily lives. Likewise, how many of us today can work or be educated without computers or access to the Internet? How many jobs are left that are truly devoid of some form of digitalization?

Since the early 1990s, the definition of the digital economy has evolved based on the existing technology trends, as well as the level at which technology penetrated different business tasks, products and services. By the mid-1990s the digital economy was a largely abstract term associated mostly with the emergence of the internet. Some saw it as the new networking of humans enabled by technology. Others as the convergence of computing and communication technologies that enabled e-commerce. Still others defined it based on its ICT infrastructure foundations.

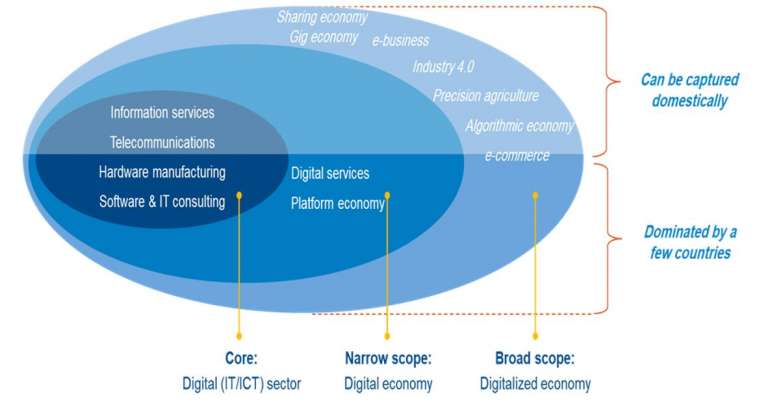

Figure 1: The evolving “Digital Economy” definition – Core, Narrow and Broad

Today, as digital technologies rapidly evolve and becomes ubiquitous, it is widely agreed that the digital economy encompasses all those definitions and more. It surely goes beyond the traditional ICT sector now and refers to a broad range of economic activities that use digitized infrastructure, data and knowledge as key factors of production or value creation. The digitalized economy. But that widening definition as in figure 1 has created multiple measurement challenges.

Our current system of national accounting of economic activities (and its most commonly known measure, Gross Domestic Product) is not well set-up to adapt to this. Gross Domestic Product (GDP) was devised in a highly industrial age and its sectoral composition reflects that.

These issues are also compounded by the fact that much digital media is notionally consumed for free, so these services go largely uncounted in GDP. That’s because the measure is based on what people pay for goods and services. If something has a price of zero, then it typically contributes zero to GDP.

Currently, estimates for the national digital economy vary across countries and are inconsistent in measurement. For example, the United States Bureau of Economic Analysis (BEA) released estimates of the digital economy’s contributions to the overall U.S. economy in April 2019. They suggest that the digital economy in the United States accounted for 6.9% of current-dollar gross domestic product in 2017, up from 5.9% in 1997. An increase of only 1% over 20 years.

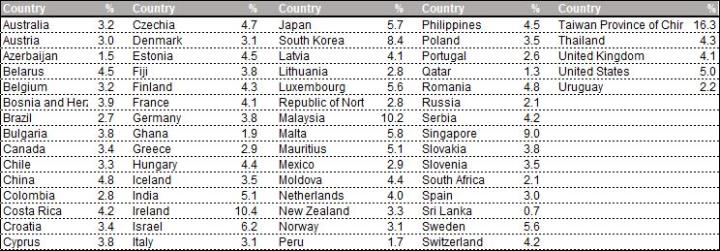

UNCTAD provide cross-country estimates through a mix of methods, predominantly using 2-digit ISIC codes from national accounts data (pertaining mostly to the ‘core’ definition of the ICT sector) and the European Commission’s Prospective insights on R&D in ICT (PREDICT) database, which features ICT sector value added and employment data for 40 economies. An obvious problem with the approach is that it suggests that leading ICT hardware manufacturers and exporters such as Malaysia and South Korea have larger shares of their GDP derived from digital value added than others. Intuitively the values for the digital economy across countries also seem too low as a share of overall GDP, given the clear centrality of digital inputs and outputs in many of our current economic activities.

Figure 2: ICT Value Added % of GDP 2017 sample of countries

The ‘broad’ definition for the digital economy includes both the ICT sector and parts of traditional sectors that have been extensively integrated with digital technology (finance, retail, entertainment etc.). The G20 has begun to embrace the broad concept of measurement, which would greatly increase the contribution of digital to overall GDP. In 2019 it defined the digital economy as “a wide range of economic activities that includes using digitized information and knowledge as the key factor of production, and modern information networks as the important activity space.” However, work on an agreed accounting methodology remains ongoing.

The China Academy of Information and Communication Technology (CAICT) provides the broadest measures of the digital economy of all current methodologies. CAICT suggest that the digital economy currently comprises 40% of China’s GDP, compared to around 60% for the United States, the United Kingdom and Germany, 46% in Japan, and around 20% in Brazil, India, and South Africa.

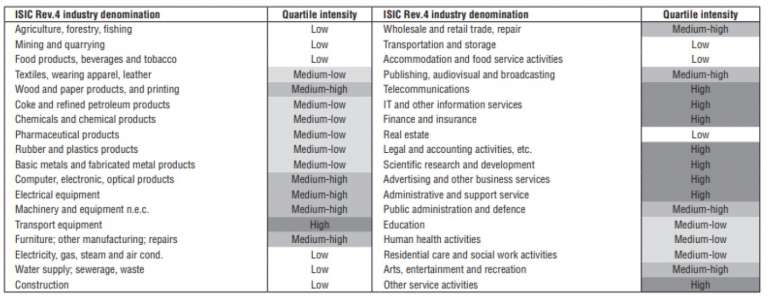

The OECD has proposed an elegant solution by taking a taxonomy of the existing GDP national accounting framework across ISIC 4 industry definitions and applying simple judgements on current digital-intensity (see figure 3). From this, appropriate shares/weights could be applied by economic sector on the share of digital inputs/outputs and applied across countries and then calculated comparatively across countries. It does of course assume similar levels of economic and sectoral digital development across countries though.

Figure 3 Taxonomy of traditional GDP by output measurement sectors by digital-intensity

While there is much discourse then of the ‘digital economy’, we still find it difficult to define it. Let alone assign a cash value to it and gauge changes in it over time.

While there is much discourse then of the ‘digital economy’, we still find it difficult to define it. Let alone assign a cash value to it and gauge changes in it over time.

But it’s really vital that we find an agreed way to do so soon. Policymakers use GDP data to help them make a wide range of decisions on national priorities for infrastructure spending, education, research and development and a myriad of other issues. If we are systematically under-reporting or certainly mis-measuring the contribution and impacts of digitalization, those decisions are being made with a poor understanding of what’s really happening in our economies.

Disclaimer: Any views and/or opinions expressed in this post by individual authors or contributors are their personal views and/or opinions and do not necessarily reflect the views and/or opinions of Huawei Technologies.

Leave a Comment